+11% rides per

user in Brazil

Driving cashless growth through Pix, Brazil's most popular payment method.

Systems, not screens. I design products wherewhere a thousand small decisions read as one.

Driving cashless growth through Pix, Brazil's most popular payment method.

Launching cashless payments for drivers who got paid in cash.

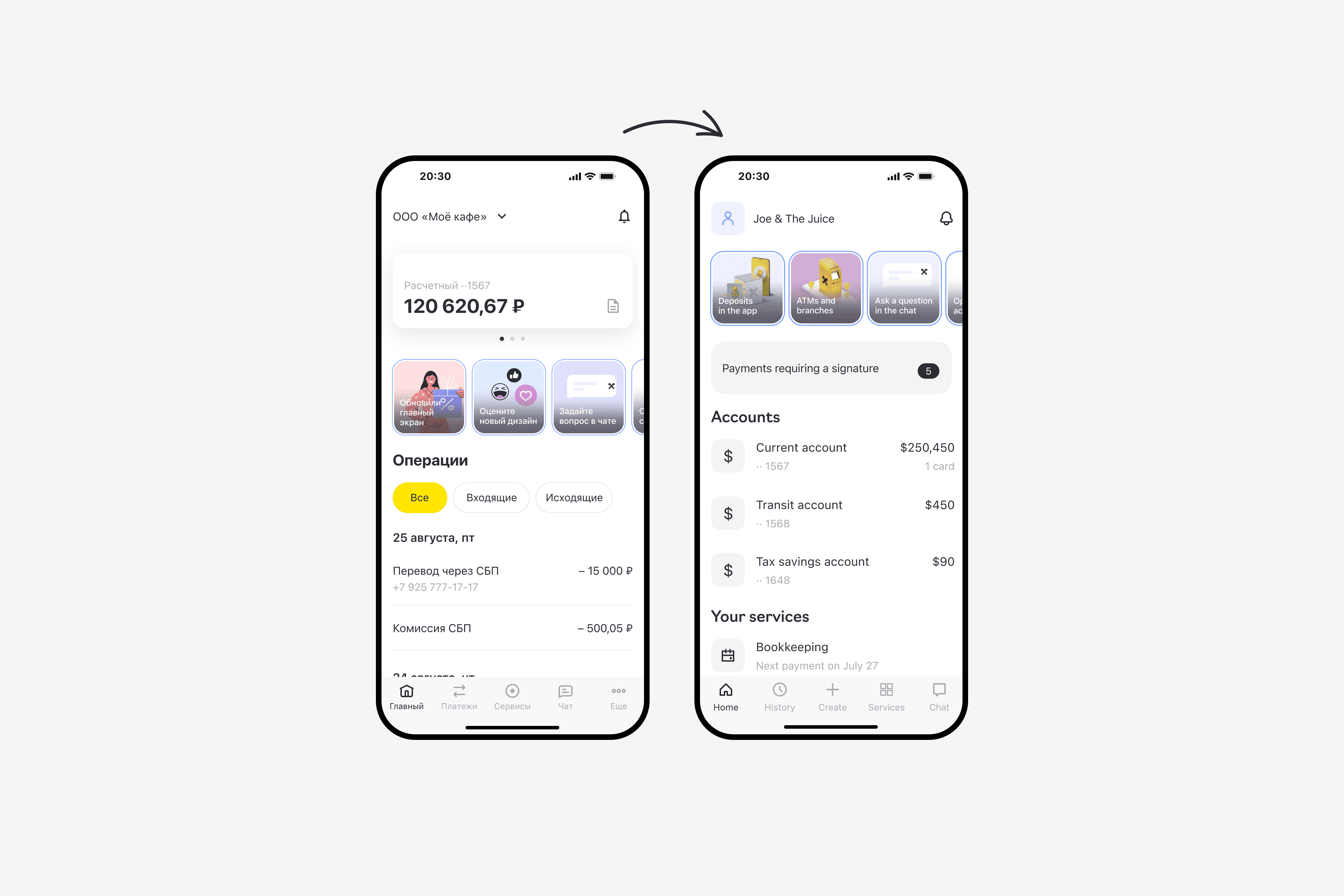

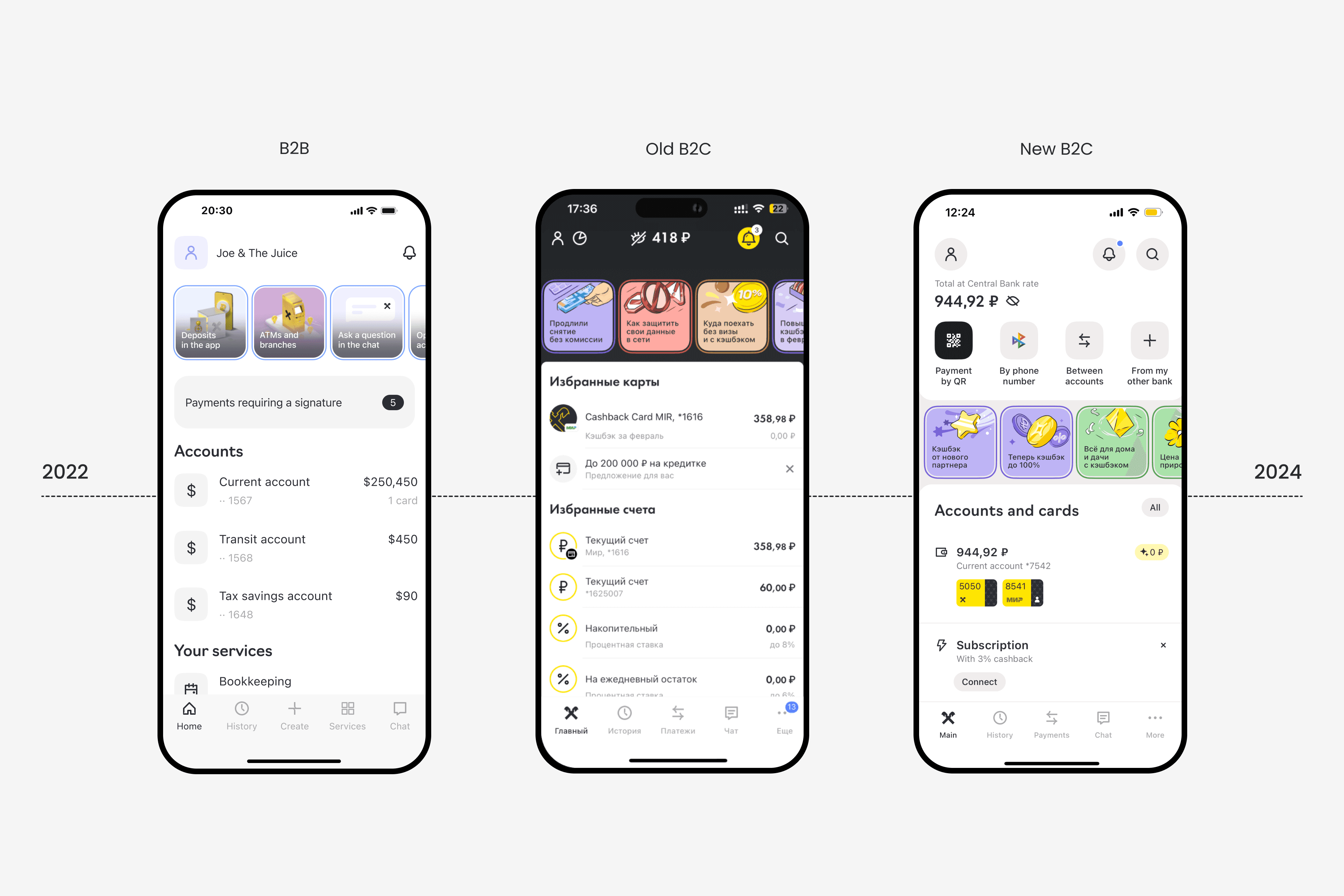

A new architecture to move web users to mobile and support future growth.

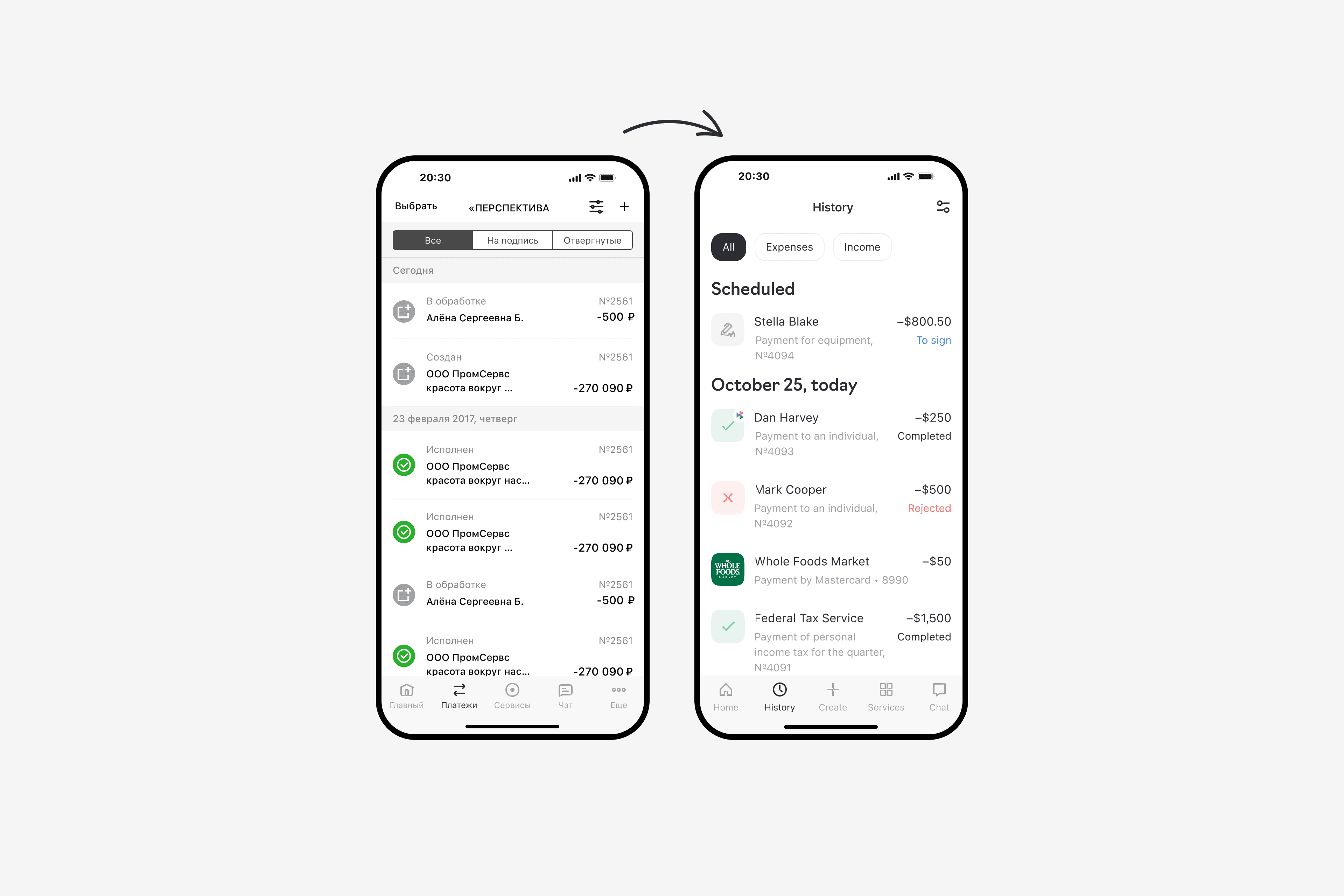

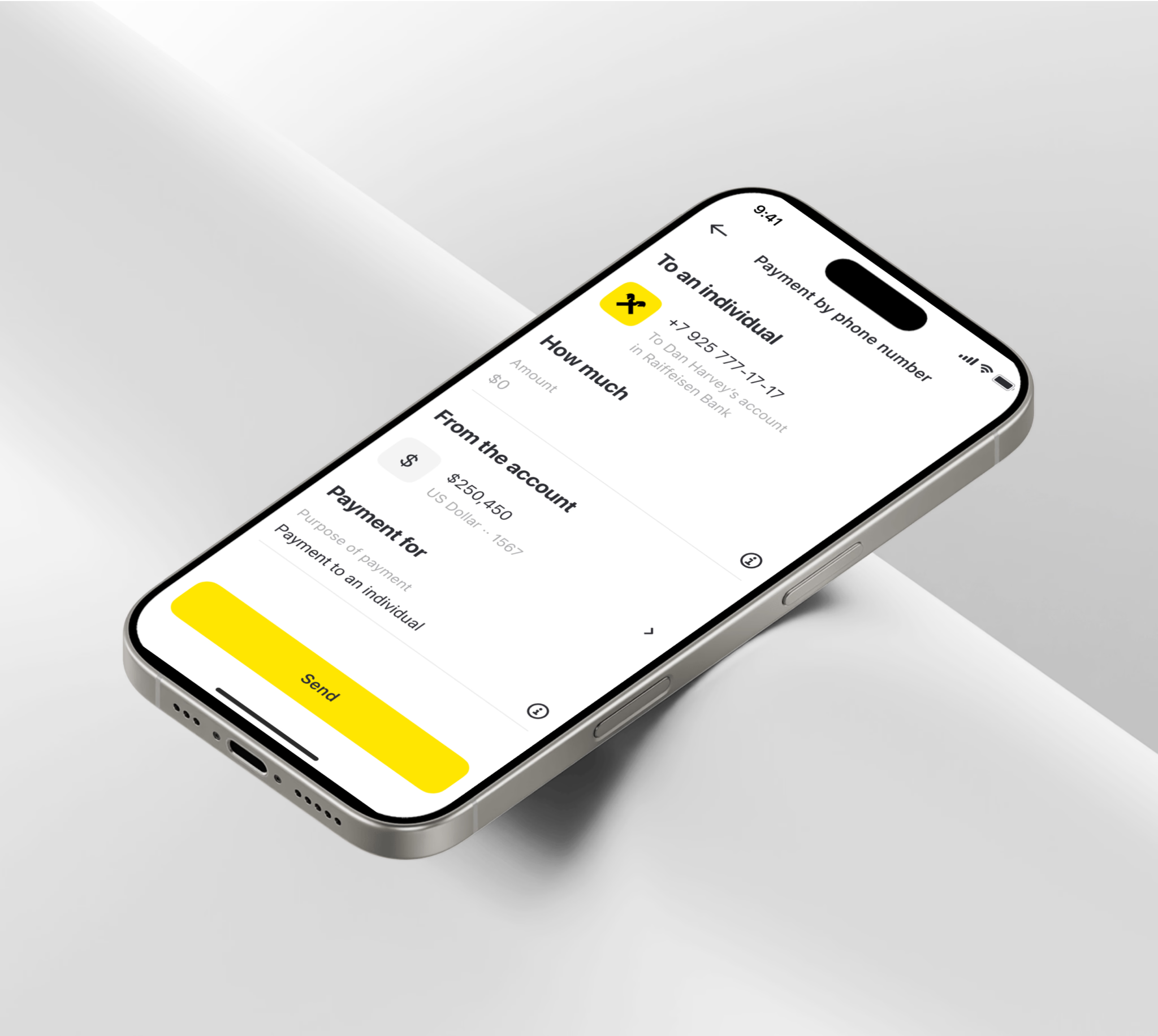

Replacing a three day wait with instant 24/7 transfers.

I have an academic background in the arts, specializing in environmental design, where I learned to see every detail as part of a larger system. That mindset still shapes how I design digital products today, connecting every touchpoint into a coherent end-to-end flow.

For the past 8+ years, I've worked across fintech, mobility, marketplaces, banking, and payments, turning complex business problems into simple, intuitive experiences.